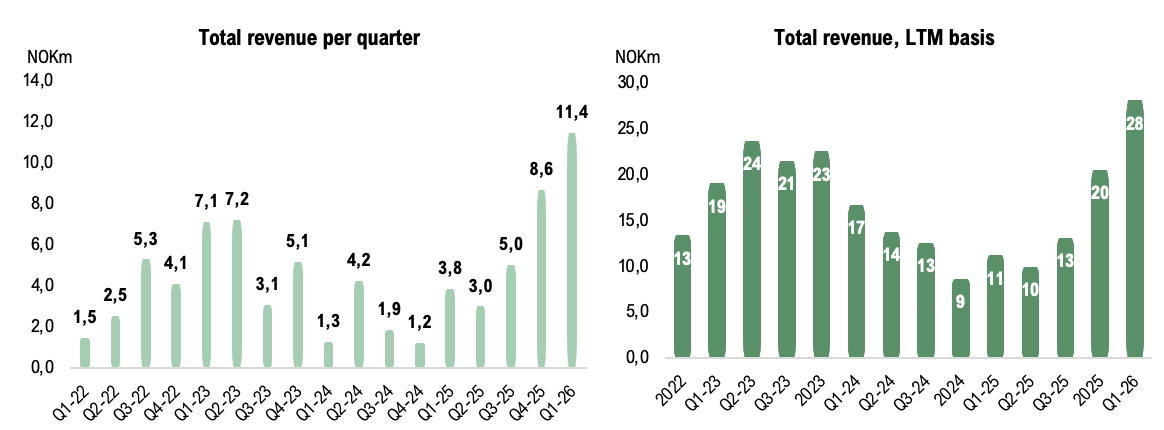

poLight ASA (“poLight” or “the Company”) published on April 29, 2026, the Company’s quarterly report for the first quarter 2026. The quarter was characterized by sustained commercial activity within AR/MR development programs. Total revenues of NOK 11.4m represented an all-time high for the Company in one quarter, supported by elevated non-recurring engineering (NRE) revenue and continued AR/MR-related deliveries. Operating expenses remained elevated, in line with poLight’s communicated strategy to scale the organization ahead of potential consumer commercialization milestones. The following are some key financial metrics that we have chosen to highlight in connection with the report:

- Total revenues of NOK 11.4m (3.8) in Q1-26 – representing a new all-time high, supported by NOK 4.2m in NRE-related revenue

- Gross profit of NOK 7.9m (1.3), corresponding to a gross margin of approximately 69%, supported by the high NRE share and a comparatively low COGS base

- EBITDA of NOK -21.7m in Q1-26 (-25.2) – reflecting continued investment in scaling and qualification programs, with an improved gross margin contribution offsetting higher operating expenses

- Cash position of NOK 261.7m at the close of the quarter (NOK 284m at year-end 2025)

Summary

poLight delivered a strong Q1-26 report, with revenues of NOK 11.4m representing a new all-time high and a YoY increase of approximately 197%. As highlighted in our preview comment, communicated orders with stated Q1-26 delivery amounted to approximately NOK 10.1m, broadly in line with our expectations, while the reported outcome came in moderately above this level. The revenue composition confirmed our prior view that a meaningful share would relate to NRE work and that underlying volumes would remain comparatively low. Sale of goods came in broadly in line with the previous quarter at NOK 7.2m (7.8m in Q4-25), while rendering of services grew materially to NOK 4.2m, indicating sustained high activity within the Company’s ongoing customer projects.

A particularly notable development during the quarter was the operationalization of the Strategic Partnership Agreement with Q Tech, where NOK 3.0m of NRE-related revenue specifically related to poLight’s support for the establishment of Q Tech’s TLens® production and test line, addressing key OEM requirements around supply chain robustness and scalability. AR/MR-related deliveries accounted for approximately 66% of total quarterly revenue, while the post-quarter dialogues around potential co-financing of further TWedge® development reinforce the broader engagement intensity across both poLight’s product platforms.

Gross margin developed favorably, supported by the high NRE share, while EBITDA improved to NOK -21.7m (-25.2 in Q1-25), driven by the NOK 6.6m higher gross profit contribution. poLight ended the quarter with a cash position of NOK 261.7m, retaining meaningful financial flexibility to continue executing on strategic priorities.

With the operationalization of the Q Tech partnership, continued AR/MR-related order activity, and strategically relevant developments around TWedge®, poLight maintains commercial momentum across multiple progressing optionalities, although the timing of formal design-in conversion within consumer AR/MR remains the principal value driver to monitor going forward.

Revenue Outcome Reflects Continued AR/MR Activity and Q Tech-Related NRE

During the first quarter of 2026, poLight reported total revenues of NOK 11.4m (3.8), corresponding to a YoY increase of approximately 197% and a QoQ increase of approximately 33% versus the previous quarterly record of NOK 8.6m in Q4-25. Total revenues consisted of sale of goods of NOK 7.2m and rendering of services of NOK 4.2m. The latter reflects elevated NRE activity during the quarter, with NOK 3.0m specifically attributable to poLight’s support for the establishment of Q Tech’s TLens® production and test line under the Strategic Partnership Agreement announced in 2025.

As highlighted in our preview comment, communicated orders with stated Q1-26 delivery amounted to approximately NOK 10.1m, broadly in line with our expectations. Consistent with our prior view that a meaningful share of these orders would relate to NRE work alongside TLens® samples, the reported revenue composition confirms that underlying volumes remain comparatively low. At the same time, engagement intensity within customer development programs has continued to increase. Sale of goods of NOK 7.2m came in broadly in line with the Q4-25 level of NOK 7.8m, indicating a stable underlying delivery base, which combined with the strong development in rendering of services overall reflects sustained high activity within the customer projects currently being pursued.

The growth was primarily driven by TLens® deliveries into AR/MR development programs, in particular under the NOK 5m purchase order announced on October 13, 2025, supporting a top-tier U.S. consumer electronics OEM in the design of a TLens®-based camera for AR applications. According to CEO Øyvind Isaksen, AR/MR-related deliveries accounted for approximately 66% of total quarterly revenue, with industrial and healthcare contributing approximately 24% and 10% respectively, reinforcing AR/MR’s increasing commercial weight relative to the Company’s broader pipeline.

Post quarter, poLight announced a follow-on TLens® purchase order of approximately NOK 2.4m for an AR/MR application on April 7, 2026. According to the Company’s Q1-26 commentary, the underlying customer program is approaching an important milestone, although certain design challenges remain to be resolved. Read our analyst comment about the follow-on purchase order here. Analyst Group views the order activity during the quarter as a continued validation that poLight’s expanding AR/MR engagement is translating into tangible purchase orders, while the qualification path naturally entails technical iteration before formal design-in conversion.

Gross Margin Reflects High NRE Contribution and Favorable Mix

poLight reported a cost of goods sold of NOK 2.2m in Q1-26, which combined with an inventory obsolescence provision of NOK 1.3m resulted in a total COGS of NOK 3.5m and a reported gross profit of NOK 7.9m, corresponding to a gross margin of approximately 69%. The favorable margin development is primarily attributable to the NRE-heavy revenue composition during the quarter. NOK 4.2m in rendering of services revenue did not carry a corresponding charge through the COGS line, which is also assumed to be supported by continued development-phase ASPs on TLens® deliveries. Excluding the NRE contribution, the underlying gross margin amounted to approximately 51%, which Analyst Group views as a strong data point reflecting the quality of poLight’s product-related deliveries during the quarter.

The gross margin development should be interpreted with caution given the relatively low absolute volumes and the development-phase nature of current revenues. As poLight transitions toward consumer volume ramp scenarios over the medium term, ASPs are expected to normalize, which would likely result in structurally lower but more stable gross margins. At the same time, increased scale, improved cost absorption, and greater system-level value capture through MLens® could partially offset this normalization effect.

Cost Base Reflects Continued Strategic Scaling

EBITDA for Q1-26 amounted to NOK -21.7m (-25.2), an improvement of approximately NOK 3.5m compared to Q1-25. The improvement was primarily driven by a NOK 6.6m higher gross profit contribution, partially offset by NOK 3.1m in higher operating expenses YoY. EBITDA ex share options improved to NOK -19.6m (-23.8), supporting the view of gradually improving operating leverage at the underlying level.

For Q1-26, R&D expenses amounted to NOK 10.2m (10.4), sales and marketing expenses to NOK 7.5m (5.0), operational and supply chain expenses to NOK 7.7m (6.6), and administrative expenses to NOK 4.3m (4.5). The change in cost composition partly reflects a reclassification of pre-sales customer development support from R&D to sales and marketing effective January 1, 2026, which explains the apparent decline in R&D personnel costs and the corresponding increase in sales and marketing personnel costs. Adjusted for this reclassification, the underlying cost base continues to expand, in line with the Company’s communicated strategy to strengthen organizational capacity ahead of potential consumer commercialization milestones. Analyst Group expects operating expenses to remain elevated through 2026 as poLight continues to invest in technology development, customer-specific qualification processes and organizational readiness ahead of a potential commercial inflection.

Cash Flow and Financial Position

As of 31 March 2026, poLight reported cash and cash equivalents of NOK 261.7m, compared to NOK 284.0m at year-end 2025. Net cash outflow from operating activities amounted to NOK 18.8m in Q1-26 (-30.6 in Q1-25), reflecting both an improved operating result and a smaller change in working capital during the quarter. Working capital increased by NOK 3.1m in Q1-26, compared to an NOK 8.8m increase in Q1-25. Net cash flows used in investing activities of NOK 3.6m primarily related to investments in new equipment for the headquarters laboratory. With a continued robust cash position, poLight retains meaningful financial flexibility to remain in execution mode through the ongoing qualification cycle, where the pace of conversion from advanced qualification programs into formal design-ins and eventual production commitments remains the key variable to monitor.

Pipeline Expansion and Strategic Positioning

poLight’s pipeline continued to mature during Q1-26, with two new industrial barcode design-wins added and the total number of design-wins reaching 44 (42 in Q4-25). The reduction in planning PoCs across consumer, AR/MR, and industrial segments reflects natural progression rather than program attrition, supported by the Company’s commentary that activity within the previously communicated programs is advancing.

The reporting period coincides with continued structural development across the broader consumer AR/MR ecosystem, as outlined in our preview comment ahead of the Q1-26 report, where major OEMs including Meta, Snap and reportedly Apple continue to advance their respective smart glasses and AR/MR roadmaps. Read our preview comment here.

As poLight notes in its own outlook, autofocus capability appears to be on the roadmap for several players in the AR/MR space, although multiple AF approaches will likely coexist depending on performance requirements and cost sensitivity. This dynamic supports the strategic relevance of TLens® without implying exclusivity and reinforces the importance of poLight maintaining technological differentiation across performance-critical applications.

Within AR/MR, sustained order recurrence and the post-quarter NOK 2.4m TLens® follow-on order continue to suggest structured advancement within a defined qualification framework. Although the Company’s disclosure that certain technical design challenges remain ahead of milestone progression highlights that the qualification path naturally entails iteration.

With respect to TWedge®, the collaboration with Vitrealab announced on April 23, 2026, represents an early external validation within next-generation laser-LCoS display architectures. More notably, the Company disclosed that initial dialogue has been initiated with key OEMs to explore co-financing of further TWedge® development efforts ahead of a potential mass production product. The Company describes these discussions as multi-faceted and complex, with the final outcome difficult to assess at this stage. However, OEM-led co-financing arrangements are not uncommon in advanced component development within consumer electronics, where lead customers occasionally share NRE costs in exchange for early access, prioritization or specification influence. A successful structuring of such an arrangement would reduce poLight’s standalone development burden and could serve as a directional signal of OEM commitment to TWedge®, although the early stage of the discussions warrants caution in extrapolating outcomes. A successful structuring of such an arrangement would reduce poLight’s standalone development burden and could serve as a directional signal of OEM commitment to TWedge®, although the early stage of the discussions warrants caution in extrapolating outcomes.

In industrial and machine vision, the launch of MLens® during the quarter, combined with positive market reception at CES and SPIE Photonics West, broadens poLight’s addressable market and supports a gradual transition toward a more system-level offering with potentially higher value capture per unit. Combined with the continued pipeline maturation in AR/MR and the strategic positioning around TWedge®, poLight enters the remainder of 2026 with multiple progressing optionalities, where the timing of formal design-in conversion within consumer AR/MR remains the principal value driver to monitor going forward.

We will return with an updated equity research report of poLight.