STENOCARE published on November 9th its Q3-report for 2023. The following are some key points that we have chosen to highlight in connection with the report:

- Continued patient growth – growth in actual sales in Q3-23

- The cost-base remains stable

- Development on the market promotes investments from big pharma

Financial Development During the Period

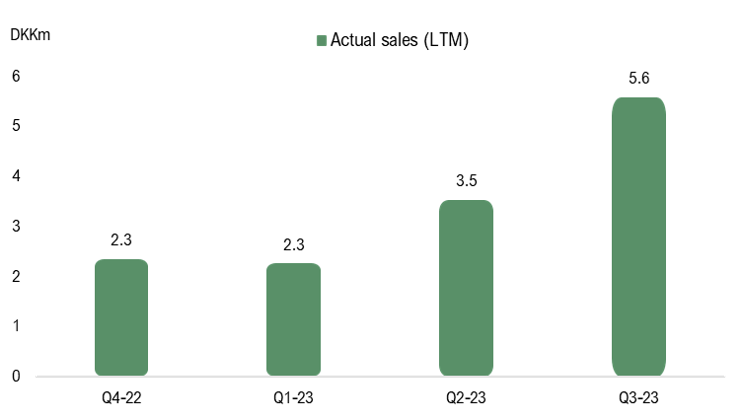

The reported net sales in Q3-23 amounted to DKK 0.2m. However, sales were negatively affected by a return of products from Norway amounting to DKK 2.1m, which was delivered in Q4-22. The pro forma adjustment consequently impacts the sales in Q4-22, but the technical adjustment is accounted for in Q3-23. Excluding the product return, sales in Q3-23 amounted to DKK 2.3m (0.3), corresponding to a growth of 686% Y-Y, albeit from low levels. The sales growth is attributable to a strong patient growth in Denmark, which data from the Danish Health Data Authority has suggested. However, the ramp-up in sales in international markets has been slower than we initially anticipated, which demonstrates the market’s inertia. However, we still believe that STENOCARE is moving in the right direction in regards to market strategy. After the quarter’s end, the company delivered its first products to Europe’s largest market, Germany, which has over 230,000 patients and projected sales of EUR 1bn in 2027.

During the third quarter, STENOCARE continued to evolve with a stable cost base, where operating costs amounted to DKK 4.9m, compared to DKK 4.6m during the same period the previous year or DKK 5.2m in the preceding quarter. EBITDA amounted to DKK -3.8m (-3.5), which was negatively affected by the return of products from Norway. Adjusted for the returned products, EBITDA amounted to DKK -1.7m, which is the best operating result since Q1-19. Based on this, we believe that STENOCARE’s costs continue to evolve as planned, moving towards the estimated break-even point by the end of 2024.

The cash flow from operating activities amounted to DKK -1.6m (-3.6), which was positively affected by a favorable development in working capital. The cash position at the end of the period amounted to DKK 5m and based on an estimated burn rate of DKK -0.7m per month, STENOCARE would be financed until early Q2-24, based on the cash position at the end of September, everything else equal. However, STENOCARE could strengthen the company’s cash position through exercise of warrants of series TO1 in December. The exercise price of Warrants of series TO1 will be a minimum price of DKK 3.21 per share and a maximum price of DKK 6.70 per share, which would strengthen STENOCARE’s cash position with between DKK 3.7-7.8m in gross proceeds. Accordingly, we see it as important that STENOCARE can strengthen the company’s cash position through TO1 to monitor the liquidity towards the estimated break even at the end of 2024 without further external capital injections.

Continued Patient Growth in Denmark

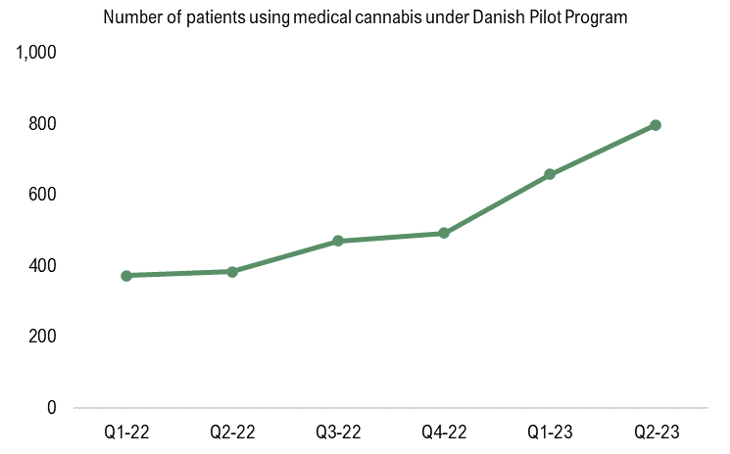

The Danish Health Data Authority has published new data on the number of Danish patients treated with medical cannabis under the Danish pilot program, which showed continued growth during Q2-23 as the number of patients grew to 798, corresponding to a growth of 90% from the same period last year. The number of patients has been growing steadily since STENOCARE introduced the company’s THC-oil and later the CBD-oil, as per the graph below. Moreover, the growth is expected to accelerate further with an approval of STENOCARE balanced oil, which is expected in Q2-24.

Development on the Market Promotes Investments from Big Pharma

In a notable development, the U.S. Department of Health and Human Services (HHS) has proposed a reclassification of cannabis to categorize it as a drug with reduced risks. This proposal sets the stage for the re-evaluation of the drug’s legal status, which could potentially expand its availability for medical and therapeutic purposes nationwide in the United States. This represents a substantial reduction in the regulatory obstacles associated with cannabis, rendering it a more attractive field for investment and scientific exploration. Furthermore, reclassification would also create opportunities for federal funding to support cannabis research, thereby reducing certain financial uncertainties.

In addition, market analyst Prohibition Partners recently published its Pharmaceutical Cannabis Report, which presents mounting evidence that adresses the effectiveness of cannabis in addressing various conditions, spanning from chronic pain to epilepsy and specific forms of cancer. The report also underscores the increasing worldwide research and development initiatives focused on uncovering the complete array of therapeutic attributes associated with cannabis.

The view of medical cannabis as a lower-risk drug, in combination with the heightened recognition of medical cannabis as a proven treatment for several symptoms, such as chronic pain and epilepsy, is expected to lead to a growing interest from big pharma companies and increase investments in the market. This is also something that has evolved in the last years as we have seen when, for instance, Pfizer acquired Arena Pharmaceuticals, a biotech company with one pipeline dedicated to cannabinoid-type therapeutics, for USD 6.7bn and Jazz Pharmceutical acquiring GW Pharmaceuticals, the developer of Epidiolex, the first FDA-authorized CBD medicine for treating children with Lennox-Gastaut and Dravet syndromes. Continued large investments from big pharma is proof of extended interest in the market and these companies may also gain advantages from more lenient regulations governing clinical trials, potentially expediting the process of introducing cannabis-derived medications to the market, hence accelerating market growth, something that is expected to favour STENOCARE.

To summarize, STENOCARE delivered sales relatively in line with our expectations (excluding returned products) and a stable cost-base. The product return from Norway is not desirable but something that we consider as a one-off occasion. Excluding the product return STENOCARE continues to deliver sales growth, driven by strong patient growth in Denmark, which is expected to continue and accelerate if STENOCARE’s balanced oil obtains approval, now expected during Q2-24. However, sales in international markets have been slower than first anticipated, which holds the growth back somewhat. We still see significant potential in these markets in the long run and expect STENOCARE to enter more markets in the coming years. A continued patient growth in Denmark, as well as on international markets, where STENOCARE now have entered Germany, Europe’s largest market, in combination with a stable cost base will be important factors to reach the estimated break even at the end of 2024.

We will return with an updated equity research report of STENOCARE.