STENOCARE published on May 2 the company’s Q1-report for 2024. The following are some key points that we have chosen to highlight in connection with the report:

- Financial development during the period

- New product approved in Denmark

- Accelerated sales growth is important for the financial position

43% Sales Growth

STENOCARE’s net sales amounted to DKK 1.2m in Q1-24, corresponding to a growth of 43% compared to Q1-23 when net sales amounted to DKK 0.8m. The gross sales, excluding product returns, amounted to DKK 1.4m, corresponding to a growth of 62%. The sales in Q1-24 included delivery of products to the Danish market, where a new product was approved for sales in Q1-24, a mixed THC/CBD oil which historically has represented +50% of sales volume in the Danish market and expected to drive the sales growth in the coming quarters as the product is available for sale since April 2024. The new product is not included in the Q1 figures but sold to the distributors after the reporting period.

With reported sales of DKK 1.2m in Q1-24, STENOCARE has a way to go to reach our annual revenue forecast for 2024 of DKK 16.5m in a Base scenario. However, it should be noted that, as mentioned in our previous updates regarding STENOCARE, sales are expected to fluctuate between quarters as a result of the company delivering products in large bulks, which means that sales are affected by in which quarter larger deliveries occur. Given the approval of the balanced oil in Q1-24, we expect growing sales on the Danish market going forward, in combination with deliveries to international markets, where sales have so far developed slower than estimated. However, a new product was launched to the Australian market during Q1-24, which is expected to be a sales driver in that market moving forward. Moreover, STENOCARE entered the German market in Q4-23, where we expect more sales in the coming quarters.

Slightly Decreased Cost Base

The operational expenses, including depreciation, amounted to DKK -4.5m in Q1-24, compared to DKK -4.8m in Q1-23, corresponding to a decrease of 7%. Sequentially, the operational expenses decreased from DKK 5.1m in Q4-23, a reduction of 12%. The sales growth in combination with the decreasing cost base, the EBITDA result improved to DKK -2.5m in Q1-24 from DKK -3.2m in Q1-23. With a slim organization and lean cost base, the estimated accelerated sales growth is expected to lead to the anticipated break even by the end of 2024.

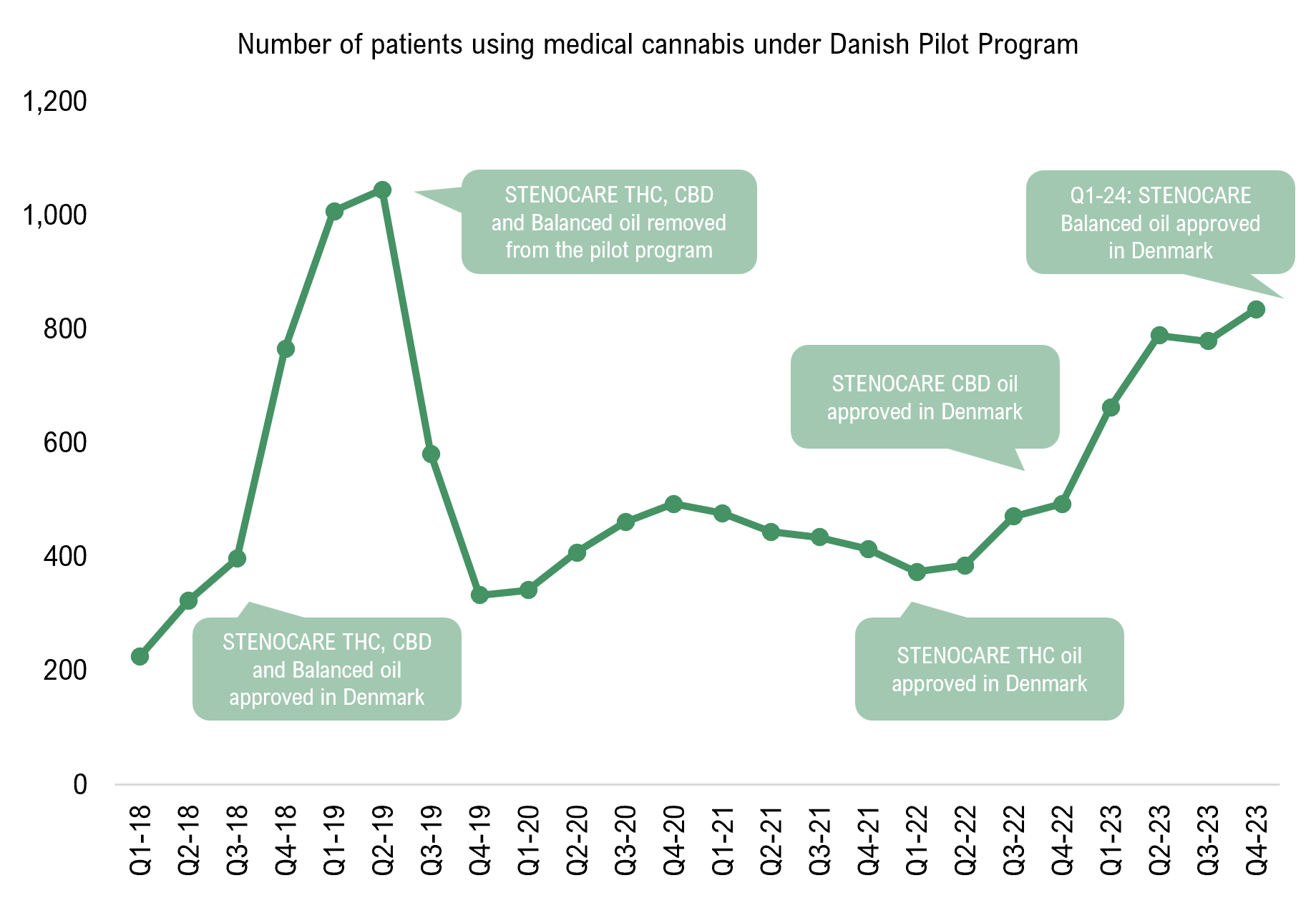

New Product Approved in Denmark

On February 26th, STENOCARE announced that a new product has been approved for sales under the Danish pilot program. The product is a mixed THC/CBD oil product, which means that STENOCARE has regained the position as the only provider of all three essential oil products under the Danish Pilot Programme: THC oil, CBD oil, and now also the new THC/CBD mixed oil. This means that STENOCARE are now back with three different products approved in Denmark, like in 2018/2019, before STENOCARE had to terminate the partnership with their then only supplier, CannTrust, and start to look for a new partner and again getting products approved by authorities, which has now been completed. When looking at the number of patients using medical cannabis under the Danish pilot program, the number of patients has historically increased after new products from STENOCARE has been approved as illustrated in the graph below. Moreover, in 2018/2019, the balanced oil represented +50% of the total sales, why we estimate that the newly approved balanced oil will accelerate patient growth in the coming quarters, thus also sales growth for STENOCARE.

Accelerated Sales Growth is Important for the Financial Position

The cash position at the end of Q1-24 amounted to DKK 2.6m, compared to DKK 9.5m at the end of Q4-23. In addition to the reported EBITDA loss, the cash position was affected by a repayment of convertible loans amounting to DKK 3.2m, which we accounted for in our comment on STENOCARE’s Q4 report. Based on the current cash position and an estimated burn rate of DKK -0.7m per month, STENOCARE would be financed until July 2024. However, the cash position can be strengthened in June by the exercise of warrants of series TO2, where 1,712,999 warrants can be exercised in the period 10 to 21 June 2024 with a price per share of the VWAP for the last 10 trading days before the exercise period beginning less 30%. Moreover, Analyst Group estimates, as previously mentioned, accelerated sales growth in the coming quarters to improve the cash flow, which we see as important to avoid further external capital raising in the future.

To summarize, STENOCARE delivered a stable report with a decreasing cost base. An accelerated sales growth is expected in the coming quarters, among other things through the introduction of new products in Denmark as well as Australia to reach our sales forecast of DKK 16.5m for 2024, which is also important for the cash position to avoid further external capital raising in the future.

We will return with an updated equity research report of STENOCARE.