Movinn published on August 25th the company’s Q2-report for 2023. The following are some key points that we have chosen to highlight in connection with the report:

- Revenues slightly below our estimates

- Costs relatively in line with our expectations

- Lower investments expected to improve cash flow as demand increases

Revenues Slightly Below our Estimates

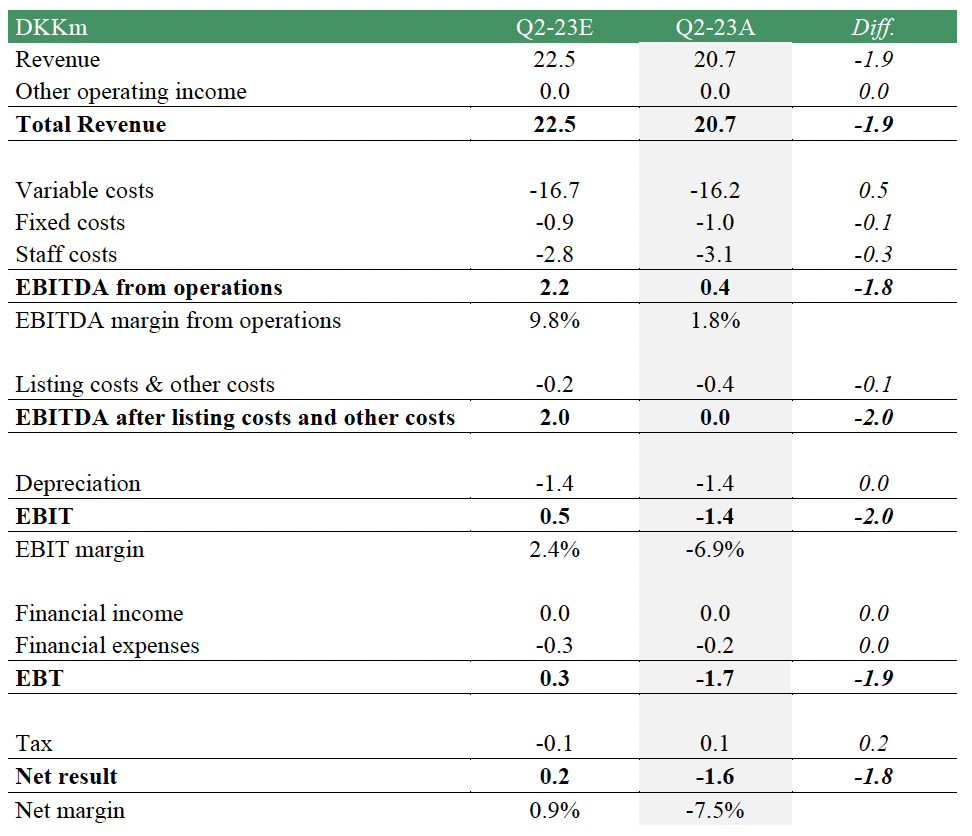

Movinn’s revenue amounted to DKK 20.7m (17.8) in Q2-23, corresponding to a growth of 16% Y-Y but 8% below our estimate of DKK 22.5m. We estimated that demand would be stronger during the second quarter due to the seasonal pattern where Q2 historically has been the strongest quarter. However, demand has continued to be slightly weaker than we expected due to an ongoing challenging macroenvironment. The weaker demand is especially attributable to the company’s two markets Aarhus and Odense, which represents approximately 33% of Movinn’s Danish portfolio, where there is currently an oversupply of apartments in Aarhus due to a high construction activity and some of Movinn’s clients have had several large projects finished in Odense at the same time, meaning that project-related clients was no longer on assignment in the city. The weaker demand is expected to continue throughout the year, which is likely to result in an update in our revenue forecast for 2023. However, the macroeconomic challenges are expected to ease during 2024, with increased demand as a result, which, in combination with that Movinn is expected to enter new markets such as Germany and Stockholm, is estimated to drive the growth in the coming years, why we still see the long-term growth-case being intact.

The revenue per unit amounted to DKK 186k in Q2-23, divided into DKK 198k on the Danish units and DKK 88k on the Swedish units, which was in line with Q1-23. The vacancy rates were also similar to the previous quarter, amounting to 16.3% on Danish units and 23.5% on Swedish units, corresponding to an average vacancy rate of 16.7% for Movinn. Analyst Group maintains that the revenue per unit remains robust, especially regarding the Danish units, considering the elevated vacancy rates driven by weaker demand. As the vacancy rates trend towards more normal levels, around 10%, through increased demand, an increase in revenue per unit is anticipated to further ascend to the upper end of the range of Movinn’s guidance of DKK 180-225k per unit.

Costs Relatively in Line With our Expectations

Movinn’s cost base was in line with our expectations in Q2-23, corresponding to an EBITDA from operations DKK 0.4m and EBITDA margin of 1.8%, compared to our estimate of DKK 2.2m and 9.8% EBITDA margin, where the difference largely is attributable to the fact that the revenue was lower than estimated. However, except from weaker demand, thus resulting in higher vacancy rates, Movinn was affected by slightly higher staff costs than anticipated, connected to hiring new staff within marketing and sales, as well as parting ways with several HQ staff members, expected to affect staff costs both in Q2 and Q3-23, but after that result in a better efficiency within the organization, leading to better profitability. Moreover, Movinn’s strategy of taking on larger projects, hence lowering the costs for adding new units, is expected to improve profitability going forward. An example of this new strategy is that the company has signed a long term lease agreement with AG Gruppen on a 94 unit development in Copenhagen. Such projects are anticipated to drive the profitability of the company in the future. The table below shows a complete comparison between our estimates and the result during the quarter.

Lower Investments Expected to Improve Cash Flow as Demand Increases

The cash flow from operating activities amounted to DKK 0.4m during the second quarter, compared to DKK -0.8m in Q1-23, where the improvement was attributable to a stronger development regarding working capital. Moreover, Movinn continues to decrease the company’s investments, in line with the strategy of a more controlled growth and focus on profitability. Going forward, as demand is expected to increase and contribute to a stronger operating margin, the lower investments is expected to improve Movinn’s free cash flow. Furthermore, when entering the German market, which is expected in 2024, Movinn is expected to replace security deposits with rental guarantees, which is expected to decrease investments further, hence contributing to improved ROIC and cash flow.

To summarize, Movinn delivered revenues slightly below our estimates due to demand being lower than expected, among other things as a result of the current macroeconomic environment, which also resulted in vacancy rates remaining at high levels, contributing to a slightly weaker bottom-line performance than estimated. However, despite the high vacancy rates, the revenue per unit remained strong, which indicates a strong revenue per unit as demand improves. Going forward, we expect an improved cash flow and ROIC through lower investments and increased demand.

We will return with an updated equity research report of Movinn.