OrderYOYO published, March 20, the company’s annual report of 2022. The following are some key financial metrics that we have chosen to highlight in connection with the report:

- Net Revenue amounted to DKK 149m – in line with our estimates

- Higher Annual Recurring revenue (ARR) than expected – ARR realized to DKK 212m, corresponding to a growth of 23% YoY

- Positive profitability trend during H2-22 – EBITDA before non-recuring costs amounted to DKK 5.1m and DKK -0.9m for the full-year 2022

OrderYOYO Delivers ARR Above our Expectations

For the full-year 2022, OrderYOYO’s ARR (annualized December MRR) amounted to DKK 212m, corresponding to o growth of 23%. The Company’s ARR was higher than our estimates of DKK 189m, which Analyst Group considers to be a result of that OrderYOYO has managed to grow both existing and new customers at the same time as the Company has delivered a churn at stable levels, despite challenging market conditions for the restaurant partners. Furthermore, due to the merger with app smart OrderYOYO has a larger share of fixed subscriptions, which amounted to 36% of the total December ARR. Analyst Group expects that the fixed subscription will contribute with more stable recurring cash flow against more volatility in usage-based subscription, especially in these difficult times where the restaurant partners are facing challenging market conditions. However, we see several benefits with the usage-based revenue model, for example, the built-in incentive structure of a falling commission rate in return for higher order volumes are beneficial for both OrderYOYO and the Restaurant Partner as increased usage is far more powerful under the usage-based subscription model.

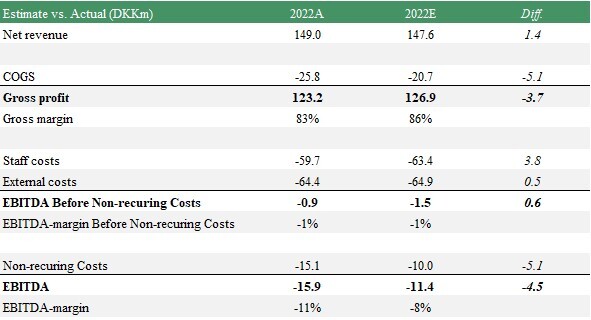

OrderYOYO’s net revenue amounted to DKK 149m in 2022 which was in line with our expectations (148), corresponding to an increase of 37% YoY. Worth noting however is that the revenue of 2022 includes six months of former app smart revenue, which is not included in 2021. Looking at the proforma net revenue (app smart consolidated full year), which is considered to be a more comparable metric, the revenue increased to DKK 184m in 2022 (165) corresponding to a growth of 12%.

EBITDA Before Other Non-Recurring Costs in Accordance to Estimates

Regarding the total staff costs, these amounted to approximately DKK -60m (-63) during 2022, corresponding to a decrease of 5%. The decrease is particular due to that part of the total staff costs in 2021 relates to IPO cash settlements and other non-recuring staff costs, totaling DKK 17m. The general staff costs increased by approximately 30% due to the merger of app smart. However, in 2022 the staff costs in percentages of net revenue decreased to 40% compared to 42% in 2021 at the same time as the Company is growing its sales, which Analyst Group believes is a proof of the high scalability in the business model. The external costs increased mainly due to the integration of OrderYOYO South, which represented 43% (DKK 64m) of net revenue in 2022 compared to 42% in 2021 (DKK 45m). Adjusted for other external costs, which includes non-recurring consultancy and transactional costs attributable to the consolidation with app smart, we believe that OrderYOYO has developed with good cost consciousness during the period. OrderYOYO has shown a positive profitability trend during the last six months, where the EBITDA before other non-recurring costs was positive in all months within the second half of 2022. This was a strong contributor to the operational EBITDA was only slightly negative during the full-year of 2022 and amounted to DKK -0.9m.

In conclusion, our view is that OrderYOYO is progressing above our estimates regarding ARR, and more or less in line with our expectations regarding topline and the general operating costs. We take a particularly positive view of, as previously mentioned, OrderYOYO showing profitability regarding the Company’s operational EBITDA during all six months of H2-22, which is a trend that Analyst Group estimates will continue.

We will return with an updated equity research report of OrderYOYO.